Even after pausing its sky-high tariffs on China for 90 days, the U.S. still has a 13% effective tariff rate, which is the highest since 1941. Moreover, prior to last week’s at least temporary de-escalation of America’s trade war with China, it was a 23% effective tariff rate. 1 Arguably, such an onerous tariff burden should hardly be a surprise, as President Trump made clear throughout his campaign that he favors restricted trade, tariffs, and economic self-reliance over free international trade.

Indeed, it is notable that, in the hours immediately preceding his inauguration, President Trump was quoted as saying "I always say 'tariffs' is the most beautiful word to me in the dictionary... Because tariffs are going to make us rich as hell. It's going to bring our country's businesses back that left us." 2

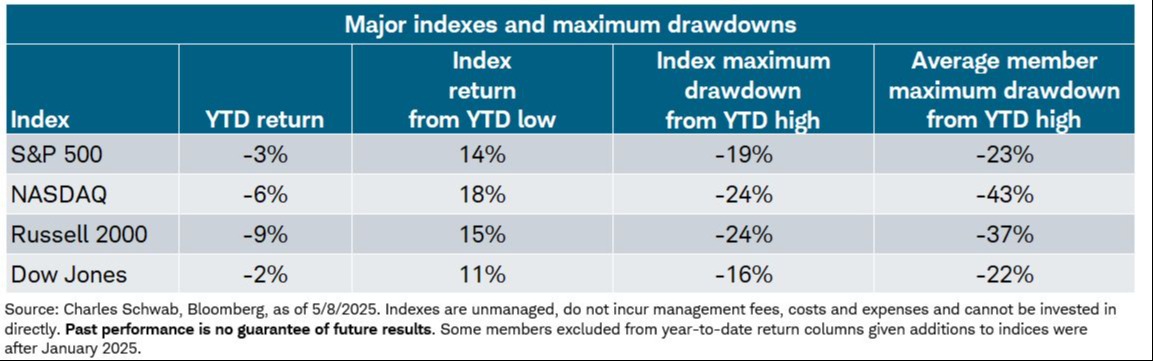

As the President openly campaigned on his administration’s current trade strategy, he has to-date maintained that “the American people have given us a mandate, a mandate like few people thought possible.” 3 and he rolled out his tariff-based trade policies both at a break-neck pace and with a global impact that few had expected. Among the places where the impact was felt most strongly was in the financial markets, where the average domestic stock (depending on the index) recently lost between 22% and 43% of its value, while foreign equity markets enjoyed their most dominant outperformance in decades.

Returns for U.S. investors investing overseas were further enhanced by a sharp decline in the U.S. dollar, which lost almost 10% of its value on a trade-weighted basis.

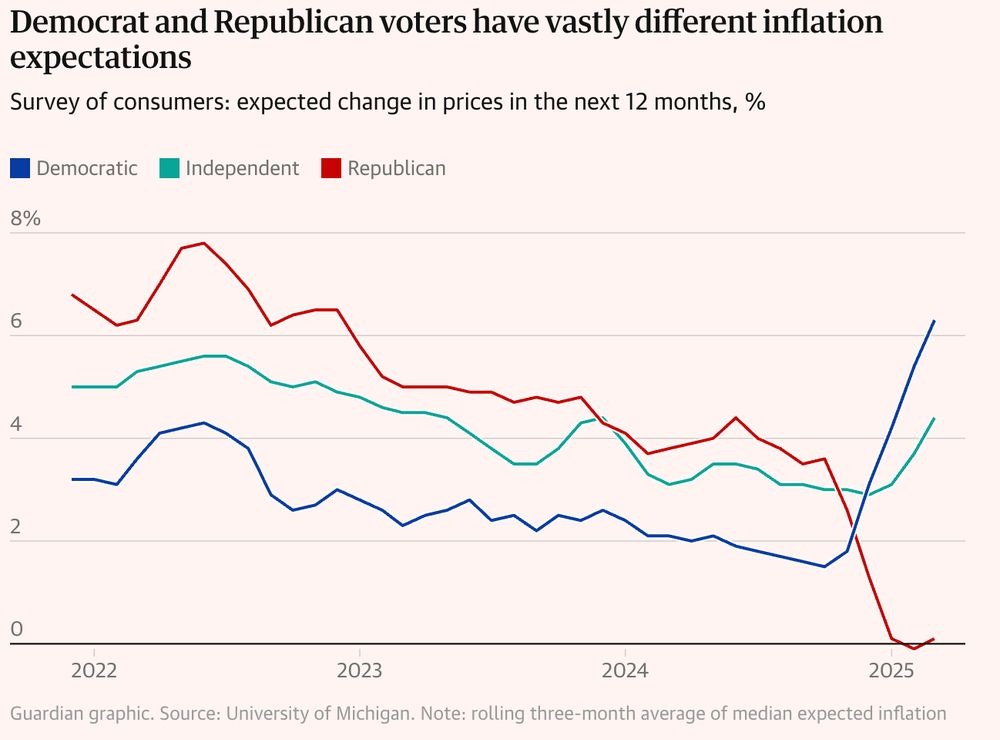

These draconian tariff policies also catalyzed a downgrade in U.S. growth and corporate profit expectations; a perceived increase in the risk of recession, and a sharp increase in inflation expectations, particularly among Democrats and, more impactfully for those Republicans in Congress facing reelection next year, independent voters. Higher tariffs are almost certain to produce higher inflation.

Whether it is due to these economic downgrades, the inflation upgrades, or the impact of the President’s tariff regime on investor portfolios, there are indications that the administration’s trade policies are losing the support of the average U.S. voter, and we think that this could have important implications for investor portfolios.

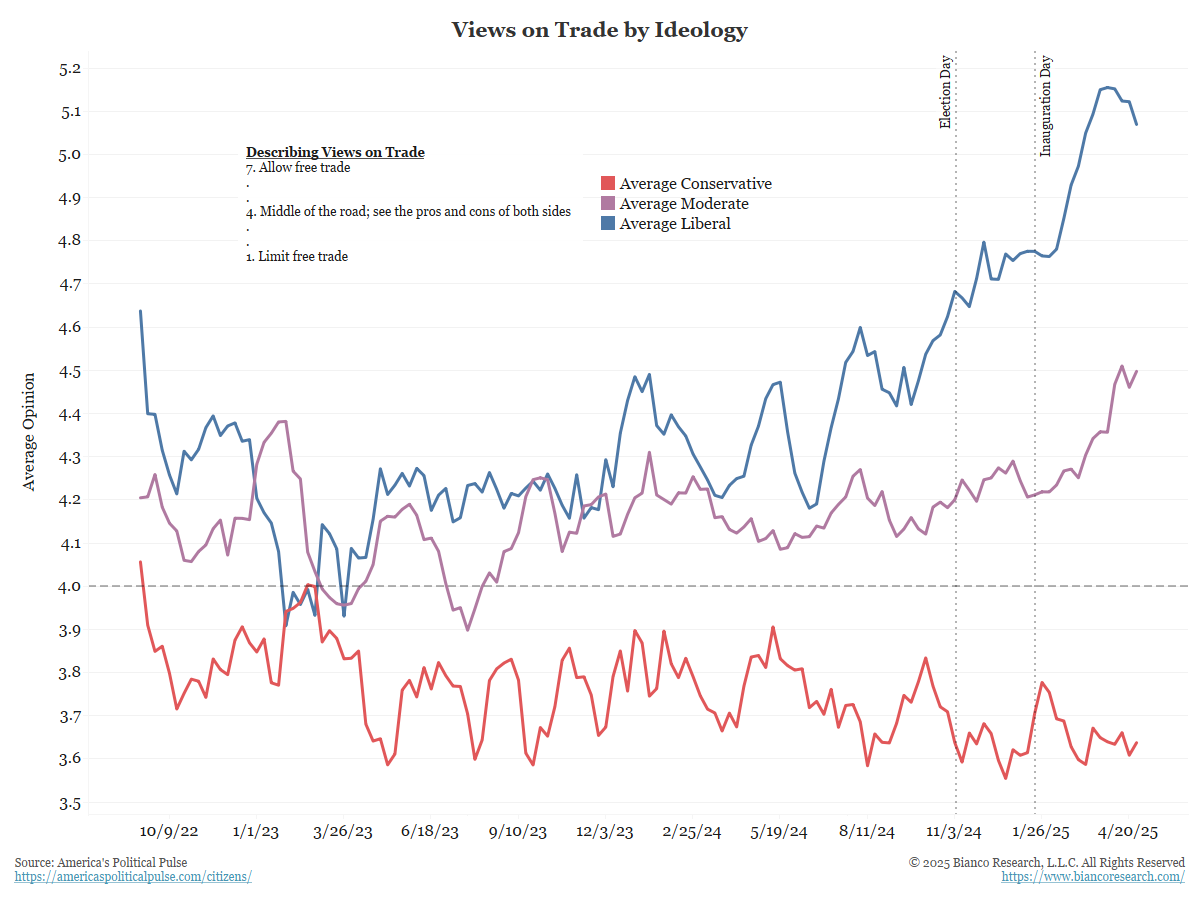

As you can see above, with the exception of Trump’s conservative base (red line), whose opinions remain largely unchanged since the election, the preferences of both liberals and, more significantly, moderates have been moving sharply in favor of free-trade, and away from President Trump’s tariff-heavy policies. Further, a Navigator Research poll conducted from April 24th to the 28th on Trump’s performance managing the economy showed that “just 40 percent of Americans approved of his handling of the economy, while 56 percent disapproved”. This represented the lowest economic rating for Trump in Navigator's tracking history. 4

From our perspective, this is causing a lessening in President Trump’s commitment to these aggressive and disruptive trade policies, and an interest in moving on to other initiatives that should be much more investor friendly, such as deregulation and the extension of the tax breaks in the 2017 Tax Cuts and Jobs Act. Hopefully, it also means a lessening of the influence of trade hawk Peter Navarro and an increased influence of trade realist Treasury Secretary Scott Bessent.

This would help to explain why the White House is now settling for what are being described as “memorandums of understanding” and/or a “broad architecture for future deals” 5 that can be reached in a day or two (like those with Great Britain and China).

Indeed, according to Politico, a “person close to the White House admitted that ‘I wouldn’t even call them deals…Basically, [it’s] an agreement that we would like to talk about doing a deal…They’re going to start rolling out a bunch of stuff that just says, you know, we’re signing something that says we’re going to start talks.’” 6

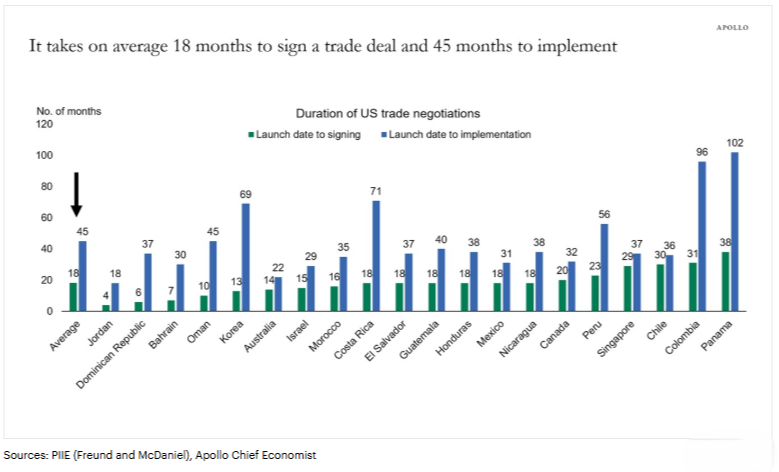

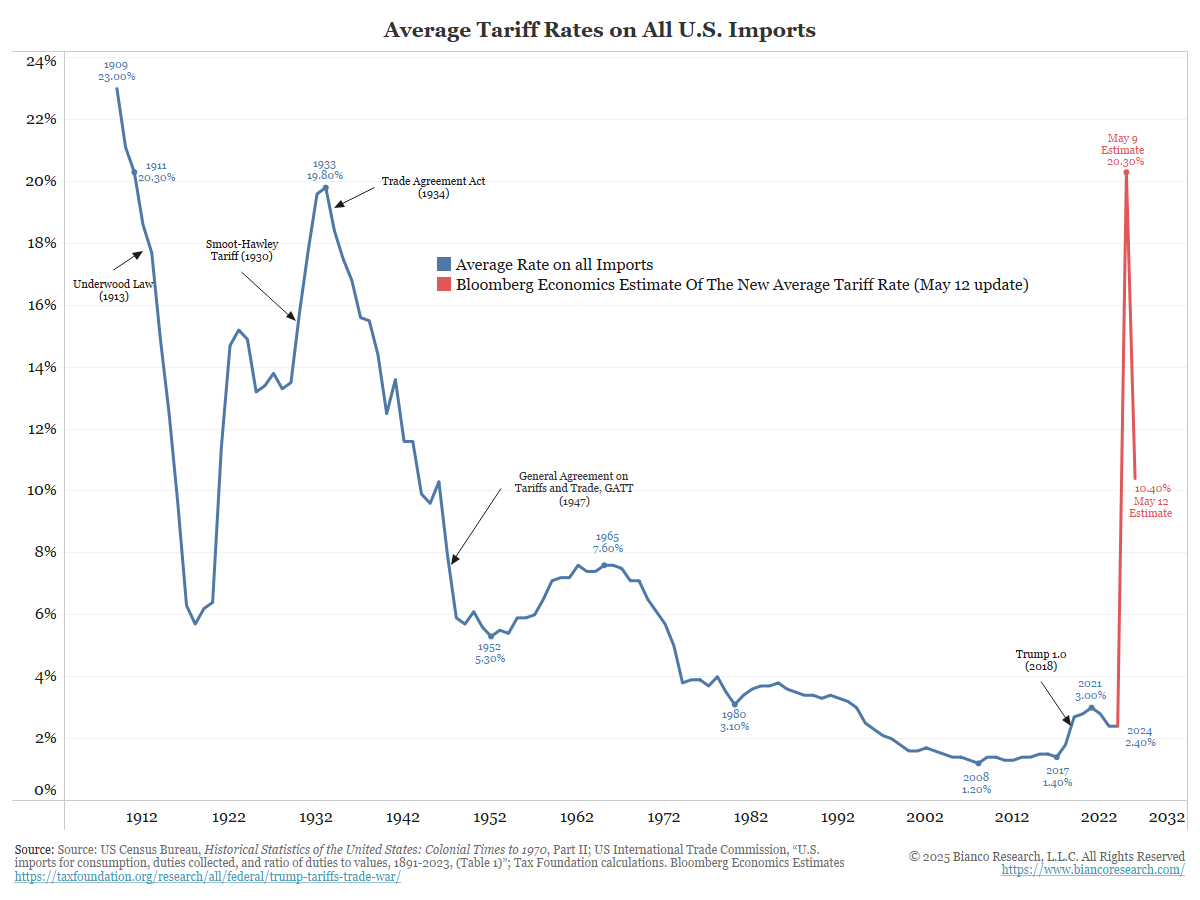

This is in sharp contrast to President Trump’s previously touted comprehensive trade agreements, which have historically taken, on average, 18 months to negotiate and 45 months to implement (see the above chart). In contrast, Commerce Secretary Howard Lutnick just announced that "over the next month or so, we are going to roll out dozens of deals". 7

While there is every reason to applaud the administration’s efforts to reduce the country’s trade and budget deficits, which were presumably two of the goals behind Trump’s pursuit of such aggressive trade policies, the extreme nature of the threatened tariffs and the dramatic uncertainty that they created are likely to do more harm than good.

As such, at least in our considered opinion, almost anything that puts them in the market’s rear-view mirror as quickly as possible and frees the President to turn his attention to his other more market-friendly policies, is ultimately quite bullish, particularly for equities.

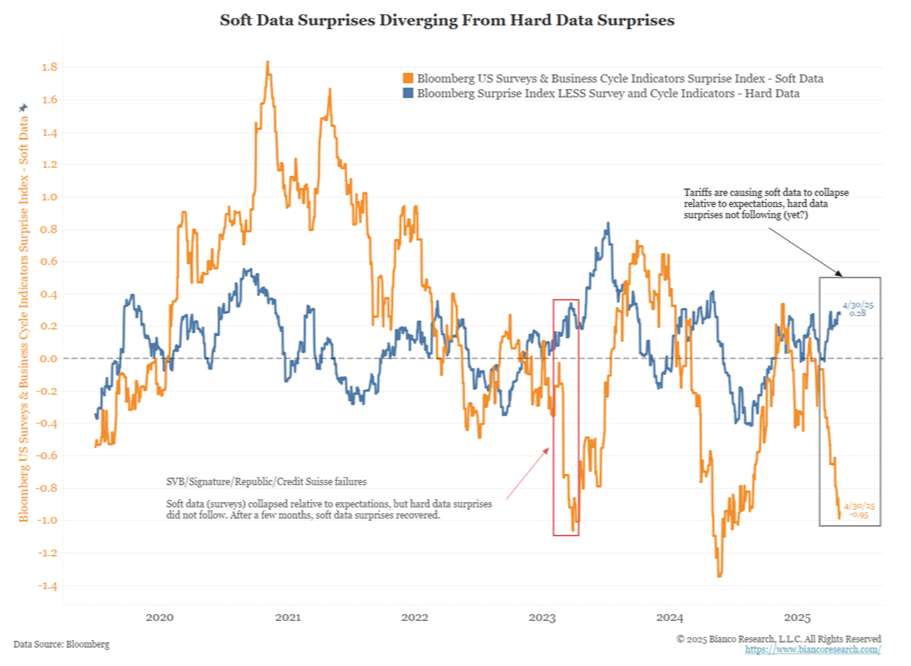

If we are correct in this expectation, then the most important question may be whether this hoped-for shift in policy takes place before the very negative economic expectations that are already being reflected in consumer, investor, economist, and business surveys (soft data/gold line above) start to bleed into the real economy and “hard data” (blue line above), which is still coming in stronger than expected. Readings below the dotted line are weaker than expected, whereas readings above the dotted line indicate stronger than expected data.

At this point, the good news seems to be that, if the threat from tariffs is significantly reduced in the very near term, it may not be too late to avoid some of the more substantial and longer-term damage implied by these very bearish polls, including hopefully avoiding an imminent recession. Indeed, as a result of the significant backing away from the brink by both the U.S. and China, “Goldman Sachs said Monday that it now expects three quarter-point rate Fed cuts starting in December instead of July, with just a 35% probability of a recession versus 45% previously”. 8

However, this more optimistic outcome is not a foregone conclusion. As was just noted by veteran business correspondent Charles Gasparino, "what the bears are saying is that the forces have been unleashed; if we don’t get cessation of the draconian nature of tariffs, we could see some nasty market turns once inflation numbers kick in, store shelves start going empty, unemployment begins to tick up, small businesses start to close because of supply chain issues." 9

Indeed, according to the Yale Budget Lab, even this temporarily reduced level of tariffs “could cost the average household $2,300 and make the U.S. economy persistently 0.4% smaller.”. 10 Moreover, while the President is suddenly “making nice” with China, he is threatening aggressive negotiations with the European Union. As he just noted, "the European Union is in many ways nastier than China, ok…We've just started with them. Oh, they'll come down a lot, you watch. We have all the cards. They treated us very unfairly." 11

As noted by Apollo Global Management’s Chief Executive Officer Marc Rowan, the Trump administration “is not wrong” in the goals it’s seeking through tariffs, but that the US risks slowing the economy if it doesn’t resolve uncertainty around trade. He went on to say that the tariff threats “have done damage to the US brand — the brand for stability, predictability, regularity [and as a result] I see us moving from what was hyper-exceptionalism to merely exceptional.” 12

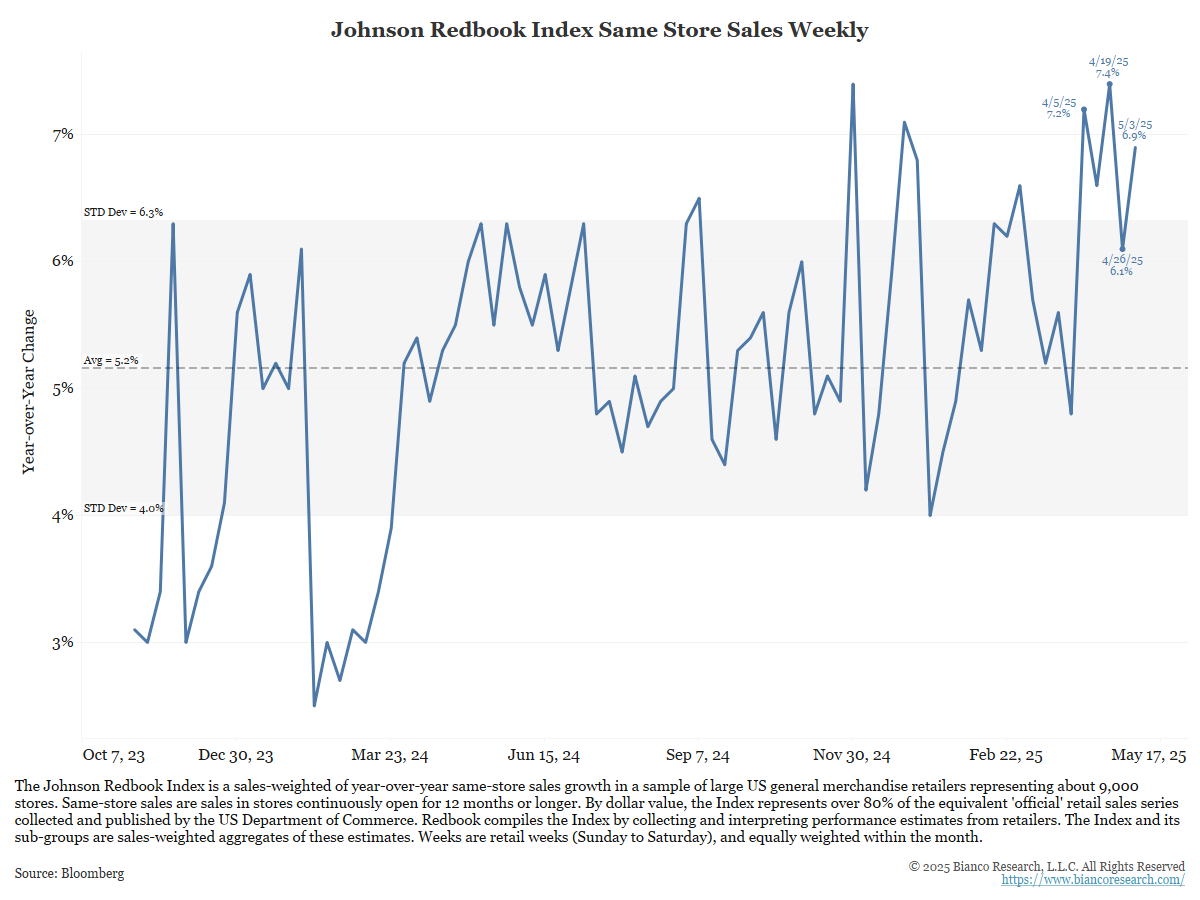

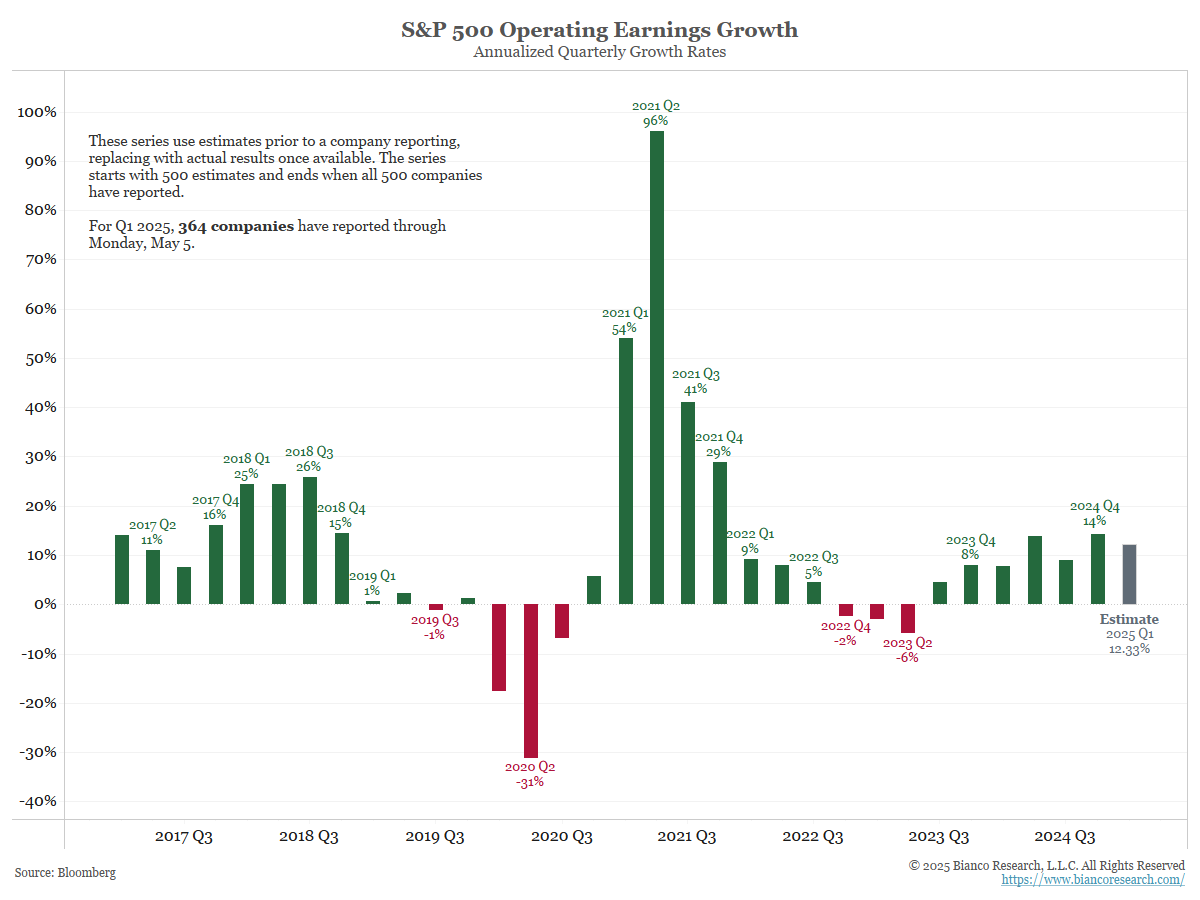

That said, with consumer spending representing more than two-thirds of the economy (GDP), we view it as a very hopeful sign that employment growth has remained relatively stable in the 150,000 to 170,000 range for monthly job increases. Of equal importance, it appears that retail sales remain quite robust despite the remarkably poor consumer confidence polls. It is also potentially encouraging that, at least thus far, estimates for corporate earnings are remaining relatively intact.

While there is still a great deal of uncertainty to be resolved, as was noted by Jeff Schulze, head of economic and market strategy at ClearBridge Investments, “it's funny what a difference a week can make. Both the positive change in trade policy and a renewed focus from the Trump administration on deregulation, tax cuts, and fiscal support is helping skew markets in a more favorable direction”. 13

At this point, most equity markets have already rebounded dramatically from their tariff-driven lows, and the tactical opportunity to “buy the dip” that we encouraged in last month’s commentary has probably already passed. That said, if this trade de-escalation continues and the economy manages to avoid a recession, there is reason to believe that 2025 could end up being the third straight year of healthy stock market returns.