When feeling threatened, a pufferfish can inflate itself to two-to-three times its normal size—an attestation that, in nature, things are not always what they seem on the surface. The same is sometimes also true of investment markets, with the U.S. stock market arguably being a prime example of this phenomenon, as a deeper dive suggests that “American exceptionalism” may not be quite as “exceptional” as it appears on the surface.

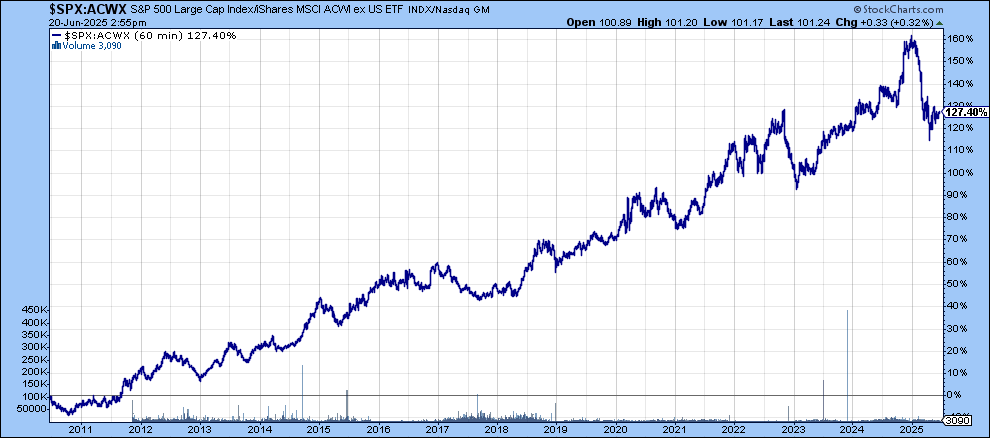

This is not to suggest that the domestic equity markets have not been an absolute juggernaut over the past fifteen years. Over that time, the Standard and Poor’s 500 Index (S&P 500) has outgained European stocks by a stunning 350% (500% versus less than 150%)1 and outperformed a broad basket of foreign stocks (the MSCI ACWI ex USA Index) by 127%. This outperformance can be seen in the following performance chart, which compares the S&P 500 Index to this broad composite of foreign stocks.

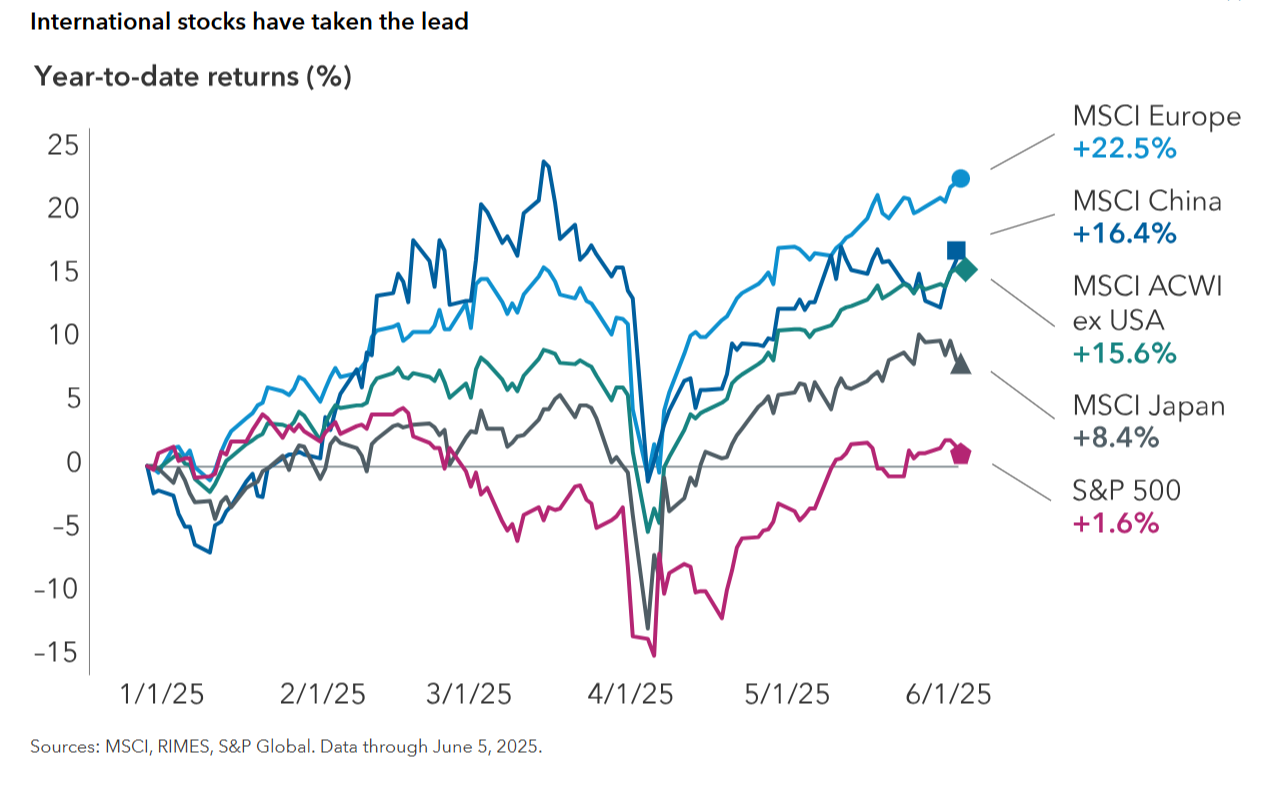

A rising line denotes U.S. outperformance, with the level of outperformance indicated on the right Y-axis. You will note a sharp reversal in this trend thus far in 2025.

So dominant has been the U.S. stock market that anyone who has only followed markets over the past fifteen years or so may be hard pressed to justify investing in any equity market outside of the U.S., particularly since investing overseas can involve additional risks.

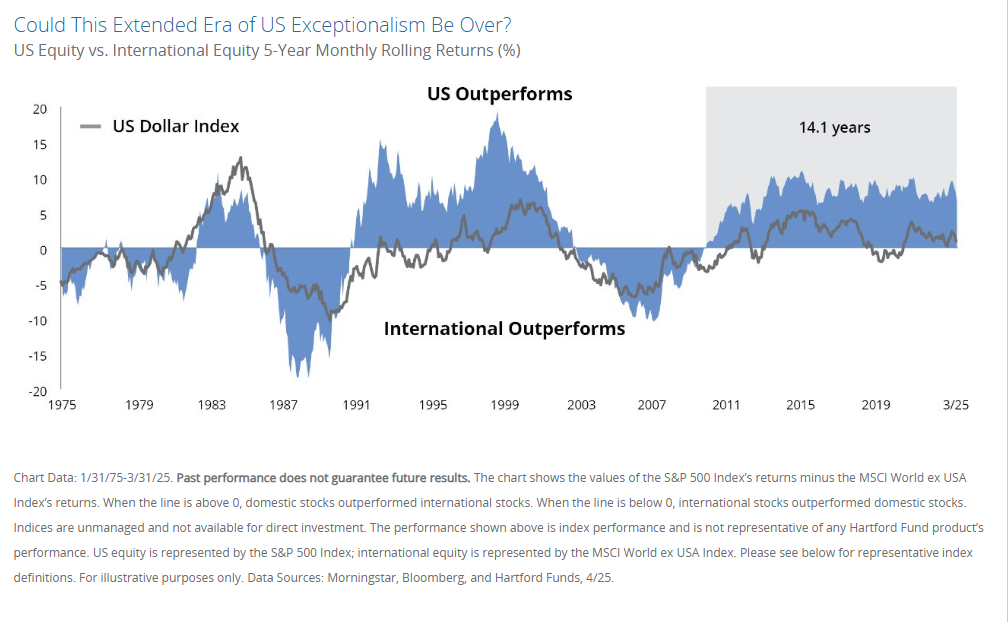

However, it is important to remember that past performance is not necessarily indicative of future results. Indeed, because American investors tend to be U.S.-centric, we sometimes forget not only that there have historically been intermittent and long-lasting cycles of under and outperformance between foreign and domestic stocks but also that, when the trend reverses, the new trend tends to last for years. For example, European stocks outperformed the S&P 500 by 90% between 1995 and 2010 (220% versus 130%)2.

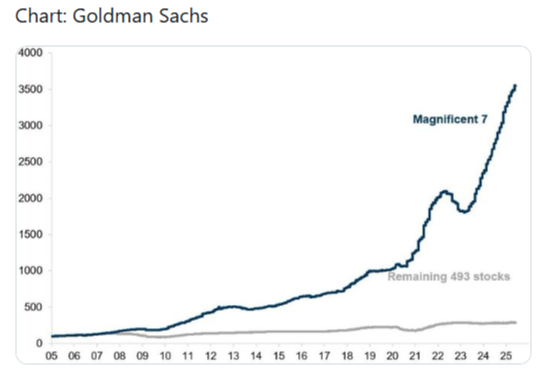

Importantly, our point is not just that we may be transitioning into a period of many foreign equity markets outperforming the domestic markets, but also that, like the aforementioned pufferfish, the U.S. stock market is arguably not what it appears on the surface, as the vast majority of the past two decades worth of U.S. equity market outperformance is attributable to only seven stocks, which are collectively referred to as “the Magnificent Seven”3.

These seven stocks, which include Apple, Microsoft, Amazon, Alphabet, Meta, NVIDIA, and Tesla, are so huge that they currently represent over 34% of the value of the entire S&P 500 Index (a collection of 503 common stocks)4. In the above chart, the X-axis shows years, and the Y-axis denotes the number of S&P 500 points gained over the period.

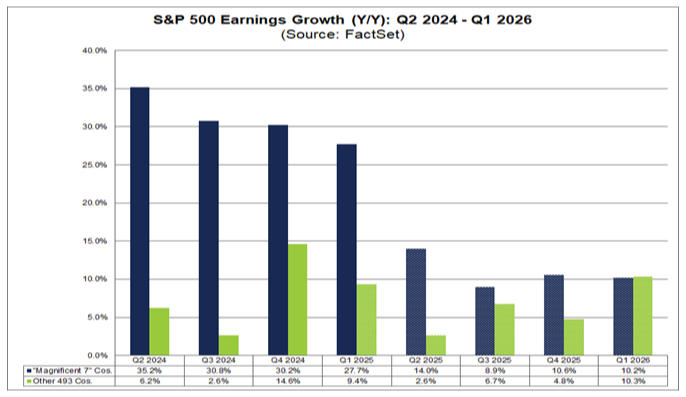

This brings us back to the caveat about “past performance”, as it is very possible that future gains in these “Magnificent 7” stocks may prove insufficient to continue driving the broad domestic stock markets higher, particularly when you consider that, if analysts are correct, one of the main factors that has driven their outstanding returns (rapid earnings growth) is expected to slow dramatically. See the above chart5.

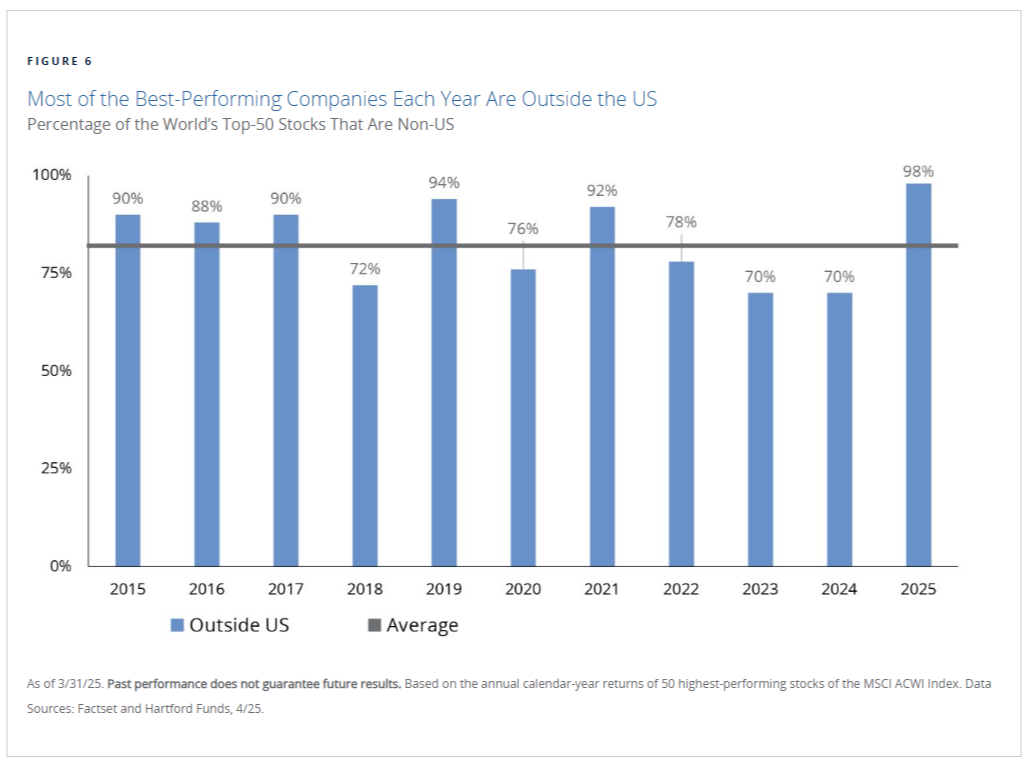

Further, as illustrated above, U.S. equity markets look even less exceptional when you consider that, over the past ten years, a ranking of the fifty top-performing stocks in the world each year reveals that the vast majority of them are consistently foreign stocks.

Traditionally, three of the most powerful determinants of stock prices are valuations, earnings growth and interest rates. At present, each of these factors arguably suggest that foreign stocks have the potential to continue this year’s relative outperformance over domestic stocks.

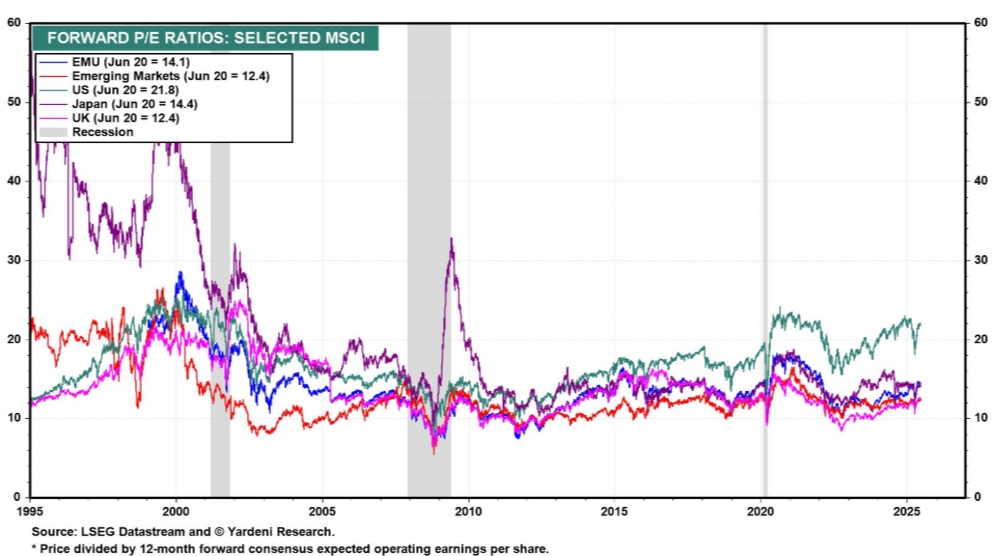

Starting with valuation, it is traditionally true that foreign stocks tend to trade at somewhat lower multiples (prices relative to earnings) than U.S. domestic stocks. That said, we are currently in an environment where foreign stock valuations are notably lower than those of U.S. stocks on both an absolute level and relative to historic differentials.

As shown above, U.S. stocks currently trade at 21.8 times the next 12 months’ worth of expected corporate earnings. In contrast, European Union stocks sell at 14.1 times earnings, emerging markets (like China, India, and Brazil) sell at 12.4 times earnings, Japanese stocks sell on average at 14.4 times earnings and British stocks sell at an average of 12.4 times earnings. In other words, an investor is currently paying almost twice as much for each dollar of U.S. corporate earnings than they are, on average, for foreign company earnings.

A highly valued market normally indicates a scenario where a great deal of good news is already being anticipated by investors and is thus already reflected in share prices. Highly priced stocks can still go higher but may require future news to be even better than the lofty expectations already being priced in. In contrast, lower valued stocks tend to be less dependent on almost everything going “right”, as only modest expectations are already reflected in their share prices. They have a “lower bar” to clear.

Put another way, because markets are forward-looking, absolute measures like “good” and “bad” are much less important than relative measures like “better than expected” or “worse than expected”. When a great deal of good news is already priced in (as is the case with many U.S. stocks), “better than expected” can become a very “high bar” to clear.

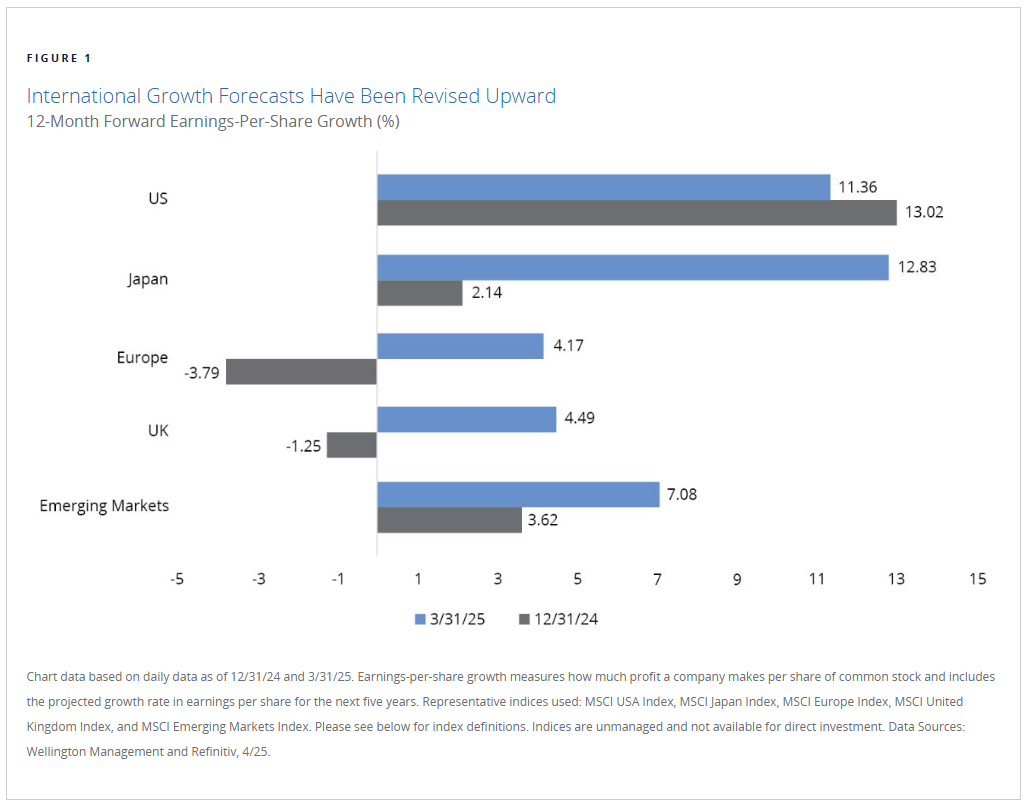

As noted, a second major driver of stock prices has traditionally been improving prospects for corporate earnings, and this too is, for a change, starting to favor the foreign equity markets, which started the year with very modest (or even downright negative) expectations for earnings improvement, and are now having those earnings growth expectations revised sharply higher. As illustrated above, many foreign markets started 2025 priced for “bad news” (the aforementioned “low bar”) and news is turning out to be better than expected.

In contrast, while U.S. companies are still expected to post impressive earnings growth, these strong growth expectations appear to have already been largely reflected in the high share prices being paid relative to earnings (the “high bar”), and now earnings expectations are being downgraded to lower than previously priced-in levels.

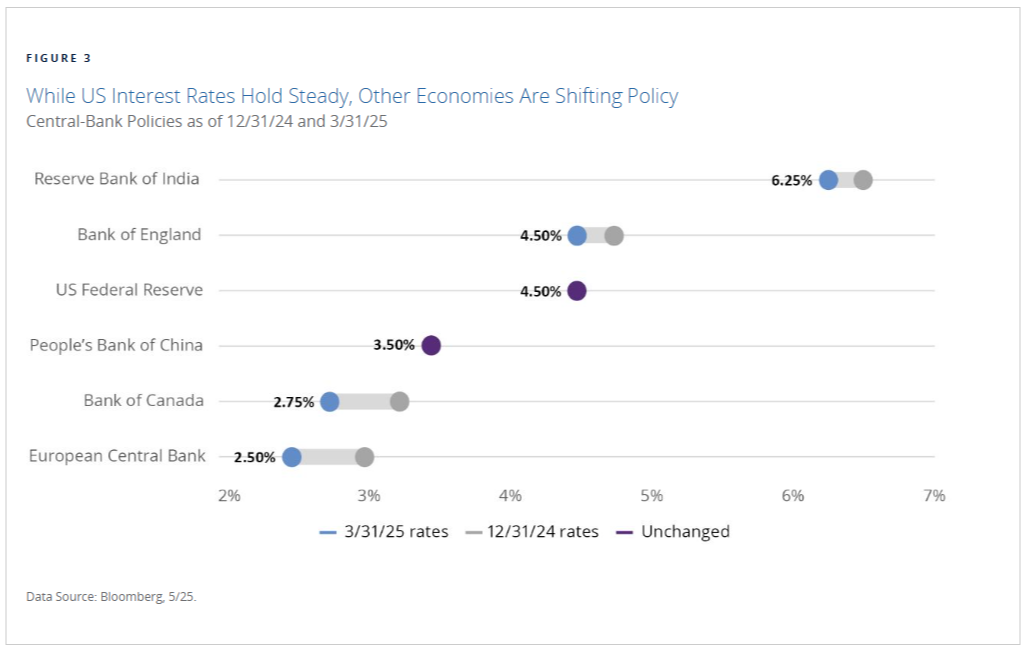

The third of the aforementioned traditional major drivers of stock prices is interest rates, and specifically the fact that low and/or falling interest rates tend to be very supportive of stock prices. Thus far, the Federal Reserve and the Bank of China are the only two major central banks that are not cutting short-term interest rates. There is some possibility that, in the U.S., this may be about to change as, over recent days, two of President Trump’s appointees to the Federal Reserve (Governors Michelle Bowman and Christopher Waller) have made comments in support of a rate cut coming as soon as the July meeting.

That said, we would be surprised by such an outcome for a variety of reasons, including the fact that, with the U.S. still facing the possible risk of resurgent inflation, we view it as very possible that the Fed could cut short-term rates only to see the markets drive intermediate and longer-term rates higher in anticipation of higher future inflation and in reaction to a lessoning of the Fed’s inflation fighting credibility. It is those intermediate and longer-term rates that most impact both the macroeconomy and the finances of American families.

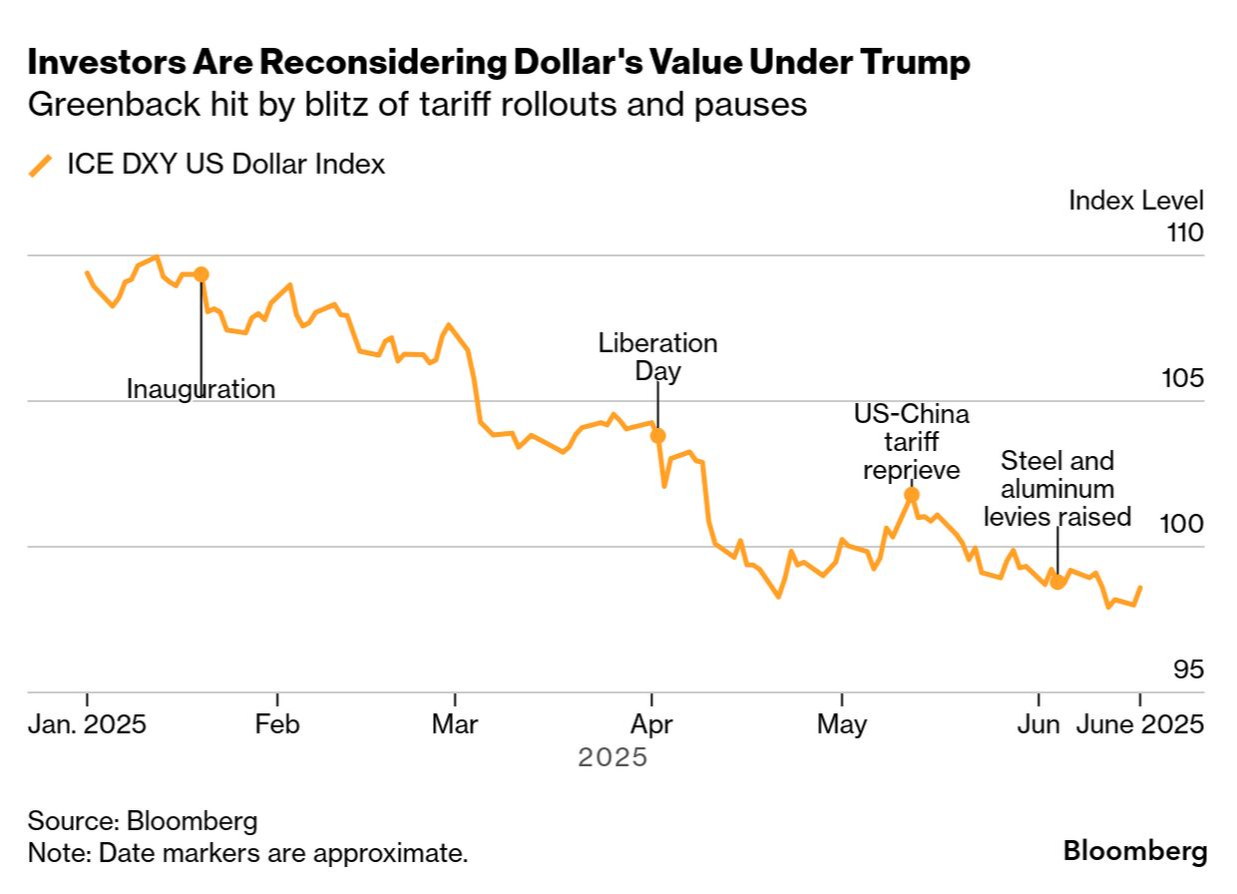

One other factor that has really benefitted American holders of foreign stocks in 2025, and which should continue to benefit U.S. owners of foreign stocks if President Trump gets his way, is a sharp decline in the value of the dollar (above) versus the currencies of America’s major trading partners. The President wants a weaker dollar because it can provide a competitive advantage to American exporters by making U.S. exports more price competitive. American investors who hold foreign securities benefit from a falling dollar because they can profit from both any nominal gains made in the securities that they are invested in and from any gains in the currencies of the countries that they are investing in versus the U.S. dollar.

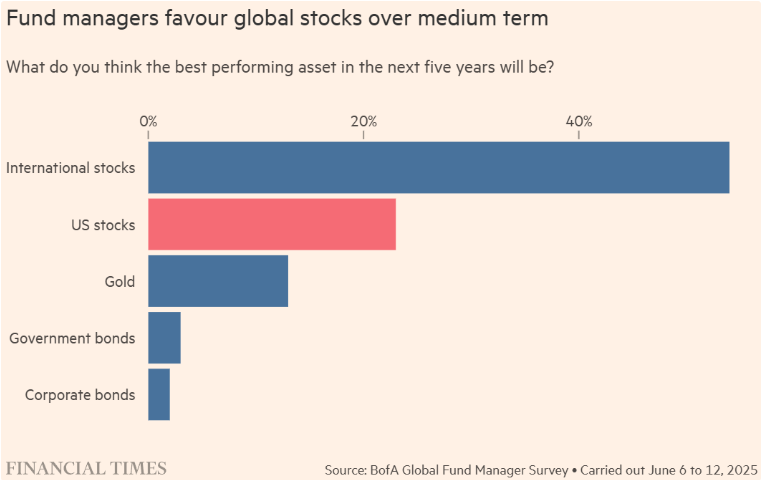

The concern is that, between a declining dollar and underperforming financial markets, foreign investors may continue to repatriate investment money back to their home countries. It is little wonder that around one-half of all fund managers surveyed in the most recent Bank of America Global Fund Manager Survey expect international stocks to be the best performing of the major asset classes over the next five years. See the above chart.

Importantly, this is not a call to sell out of all U.S. equities and move your money overseas. After all, there is a reason why U.S. equities sell at such a hefty premium. The U.S. has the largest equity market on earth, the economy remains strong, inflation is gradually being brought under control, and it is almost certainly just a matter of time before the Fed starts cutting rates and the White House moves past its disruptive trade and immigration policies and onto more market-friendly policies like lower taxes and lesser regulation.

In addition, there are certain industries, like technology, telecommunications and other innovation-based sectors, where the U.S. is dominant on a global basis.

Instead, our perspective is twofold. First of all, after a fourteen-year cycle of disappointing returns in the foreign equity markets, there is a growing array of reasons to be globally diversified. In addition to the potential for enhanced returns, foreign markets can trade very differently from domestic stocks thus potentially making them a valuable price diversifier, which could be particularly important in the current environment, when domestic stocks and bonds are trading in fairly close correlation.

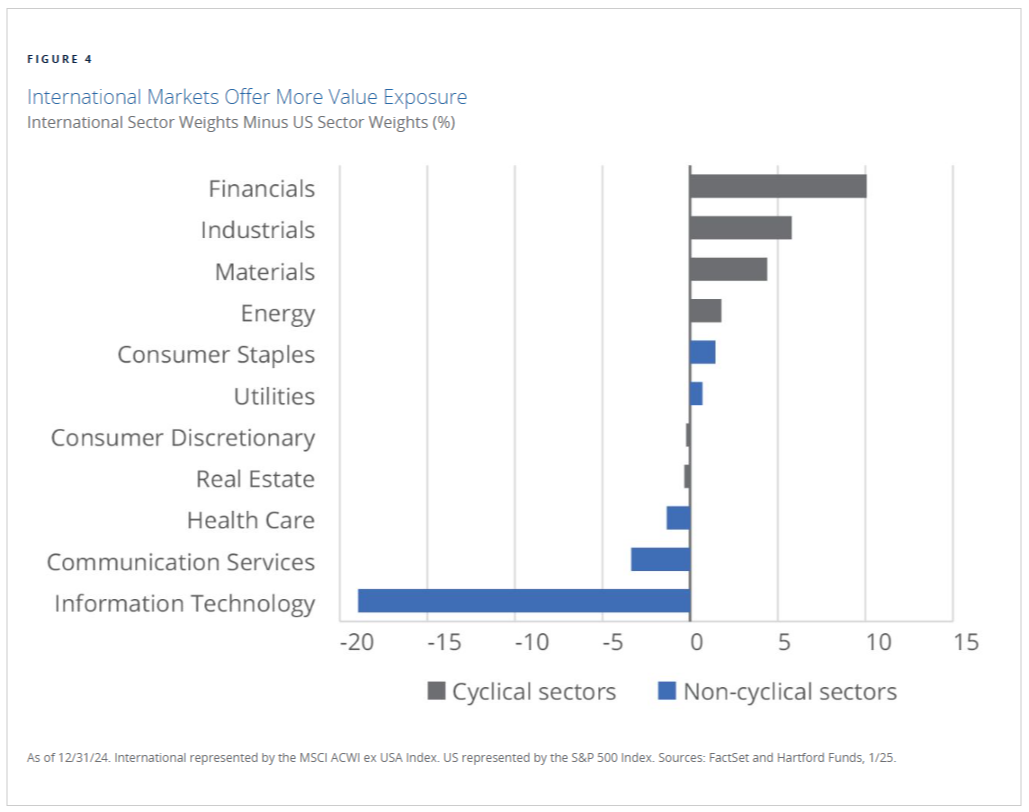

Second, we think that this might be an opportunity to pursue a different type of “barbell” strategy, where one continues to allocate to domestic equities for their portfolio’s growth exposure, but looks towards the foreign equity markets in general (and European markets in particular) to get their portfolio’s exposure to more value-oriented equities.

After all, as noted by Harry Markowitz, who is credited as the inventor of modern portfolio theory, “diversification is the only free lunch in investing”7.

Disclosures

Advisory services offered through Per Stirling Capital Management, LLC. Securities offered through B. B. Graham & Co., Inc., member FINRA/SIPC. Per Stirling Capital Management, LLC, DBA Per Stirling Private Wealth and B. B. Graham & Co., Inc., are separate and otherwise unrelated companies.

This material represents an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor.

Nothing contained herein is to be considered a solicitation, research material, an investment recommendation or advice of any kind. The information contained herein may contain information that is subject to change without notice. Any investments or strategies referenced herein do not take into account the investment objectives, financial situation or particular needs of any specific person. Product suitability must be independently determined for each individual investor.

This document may contain forward-looking statements based on Per Stirling Capital Management, LLC’s (hereafter PSCM) expectations and projections about the methods by which it expects to invest. Those statements are sometimes indicated by words such as “expects,” “believes,” “will” and similar expressions. In addition, any statements that refer to expectations, projections or characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. Such statements are not guarantying future performance and are subject to certain risks, uncertainties and assumptions that are difficult to predict. Therefore, actual returns could differ materially and adversely from those expressed or implied in any forward-looking statements as a result of various factors. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the views of PSCM’s Investment Advisor Representatives.

Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted.

Investing internationally carries additional risks such as differences in financial reporting, currency exchange risk, as well as economic and political risk unique to the specific country. This may result in greater share price volatility. Shares, when sold, may be worth more or less than their original cost.

Definitions

The Standard & Poor's 500 (S&P 500) is a market-capitalization-weighted index of the 500 largest publicly-traded companies in the U.S with each stock's weight in the index proportionate to its market. It is not an exact list of the top 500 U.S. companies by market capitalization because there are other criteria to be included in the index.

The MSCI All Country World Index ex USA Investable Market Index (IMI) captures large, mid and small cap representation across 22 of 23 Developed Markets (DM) countries (excluding the United States) and 23 Emerging Markets (EM) countries*. With 6,062 constituents, the index covers approximately 99% of the global equity opportunity set outside the US.

MSCI indexes: http://www.msci.com/products/indices/tools/

Indices are unmanaged and investors cannot invest directly in an index. Unless otherwise noted, performance of indices does not account for any fees, commissions or other expenses that would be incurred. Returns do not include reinvested dividends.

Citations

- “It’s a Scary World, but Investing Abroad Has New Attractions”, James Mackintosh, Posted 6/15/2025, https://www.wsj.com/finance/investing/its-a-scary-world-but-investing-abroad-has-new-attractions-f6e39d6b

- “It’s a Scary World, but Investing Abroad Has New Attractions”, James Mackintosh, Posted 6/15/2025, https://www.wsj.com/finance/investing/its-a-scary-world-but-investing-abroad-has-new-attractions-f6e39d6b

- “What If You Invested In S&P 500 Excluding Mag 7? Here's How NVDA, AMZN, AAPL And Others Have Performed In The Last Year”, Rishabh Mishra, Posted 6/20/2025, https://www.benzinga.com/markets/equities/25/06/46026336/what-if-you-invested-in-sp-500-excluding-mag-7-heres-how-nvda-amzn-aapl-and-others-have-performed-in-the-last-year

- “The Magnificent Seven’s Market Cap Vs. the S&P 500”, Lyle Daly, Posted 5/15/2025, The Magnificent Seven’s Market Cap vs. the S&P 500 | The Motley Fool

- ““Magnificent 7” Companies Reported Earnings Growth Above 25% for Q1”, John Butters, Posted 6/2/2025, “Magnificent 7” Companies Reported Earnings Growth Above 25% for Q1

- “From trade wars to capital wars: Section 899 could rattle global capital markets”, John Satory, Posted 6/23/2025, From trade wars to capital wars: Section 899 could rattle global capital markets - Atlantic Council

- “Diversification -The Only (Almost) Free Lunch in Investing”, Brian Schafer, Posted 5/6/2024, Diversification - The Only (Almost) Free Lunch in Investing - Greenleaf Trust