“Stagflation” is an oxymoron. It is the economic equivalent of “jumbo shrimp”, “deafening silence” and “virtual reality”. It is a portmanteau of two words that should not coexist under “normal” circumstances, as they are, at least in theory, mutually exclusive and incompatible with one another. Nonetheless, in the current economic environment, stagflation is a word that has returned as an important part of the American lexicon.

The “stag” refers to a slowing, stagnant, or even contracting economy, which normally depresses wages and asset values, while either slowing the rate of inflation (i.e., disinflation) or causing prices across much of the economy to actually decline (i.e., deflation).

In sharp contrast, the “flation” component refers to inflation, or an acceleration in wages, prices and certain asset values, which is normally associated with strong economic growth, an overheating economy (the opposite of stagnation) or an economy that is already very late in an economic cycle and/or is already running at or above full capacity.

Put another way, inflation is normally associated with a strong, mature economy, while deflation and disinflation are normally associated with a slowing or contracting economy. This incompatibility helps to explain why stagflation is such a rare phenomenon, and why it is normally accompanied/catalyzed by some massive external shock like the Arab Oil Embargos of 1973-74 and 1979, which made gas lines like the above a common sight, or the COVID pandemic of 2019-2023, which disrupted supply chains across the globe.

Could the President’s trade, tariff and immigration policies, along with a broader trend towards isolationism, protectionism, and deglobalization represent the next external shock that opens up the door for the return of these unlikely bedfellows (increasing inflation at a time of slowing growth)?

Before we attempt to answer that question, we believe that it is important to first explain some of the reasons why we believe that the answer is of such substantial importance. Two of them are obvious, as both components are undesirable. Higher inflation reduces everyone’s standard of living and erodes the purchasing power of everyone’s savings, while a slower, stagnating economy is normally associated with higher unemployment, reduced corporate profits, and fewer opportunities to grow and create wealth.

A third reason is perhaps less obvious, but arguably equally impactful, which is that it creates a conundrum for the Federal Reserve and an impediment to the fulfillment of the Fed’s “dual mandate”, which is to pursue the optimal balance between maximum employment and sustainably low inflation.

A stagflationary environment compromises the Federal Reserve’s ability to stimulate a weakening labor market by lowering interest rates, as lower interest rates are likely to simultaneously exacerbate the already problematically high levels of inflation. Similarly, the Fed is compromised in its ability to battle unwantedly high inflation by raising interest rates, as higher interest rates will further slow an already subpar economy and labor market.

What suddenly makes this topic particularly relevant is recent evidence that the trend in inflation seems to be decidedly higher, and that there has been a quite notable decline in the rate of job growth. Importantly, as discussed in our July commentary, there is an open question about whether tariffs will produce a one-time increase in prices or the start of an ongoing and increasingly inflationary trend. As is reflected in the above projection from Goldman Sachs, there seems to be an increasing expectation of a one-time boost to inflation followed by a moderation in 2026.

In contrast, concerns regarding the pace of job creation have become acute over the past three months, largely due to weakness in July and sharp revisions lower in the May and June payroll numbers, which prompted President Trump to fire Bureau of Labor Statistics Commissioner Erika McEntarfer (although Trump also accused her of distorting the numbers for political reasons).

In the early August Bank of America survey of global portfolio managers, 70% of respondents said they expect stagflation within the next 12 months 1 and, at the Jackson Hole Economic Forum on August 22nd, Former Fed Governor Roger Ferguson described the current environment as a period of "stagflation light". 2

At the same conference, Fed Chairman Powell also addressed this conundrum in his keynote speech, when he noted that “risks to inflation are tilted to the upside, and risks to employment to the downside—a challenging situation. When our goals are in tension like this, our framework calls for us to balance both sides of our dual mandate…the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.” 3 In other words, Powell is foreshadowing that, while most of the Federal Reserve is still quite concerned about inflation, the Fed is increasingly likely to cut rates at its September meeting.

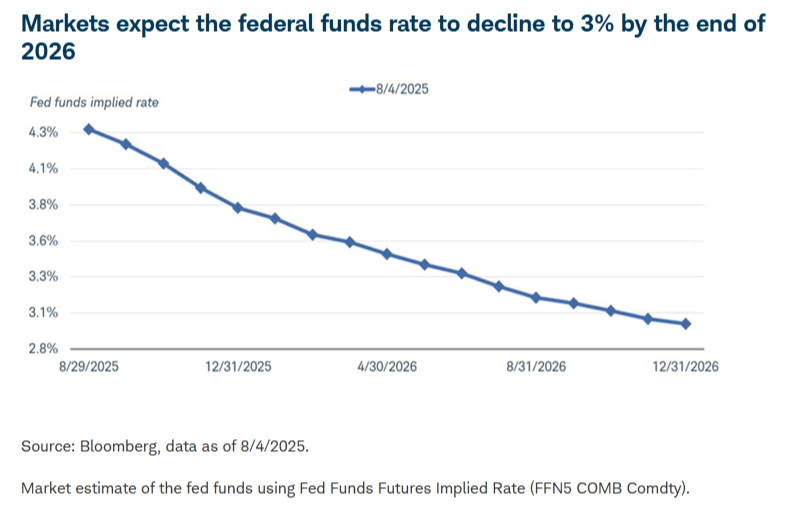

Whether such a move would ultimately be justified by economic conditions, or if it would just be indicative of the Fed finally succumbing to the relentless pressure from President Trump to cut rates, will likely be of great importance to fixed income investors as, if the markets perceive that the Fed’s resumption of rate cuts is unwarranted, it is very possible that longer-term rates (gold line, above) will disappoint investors by actually moving higher in response to lower short-term rates, based upon investor fears that the rate cut(s) will worsen inflation. This was the case when the Fed cut rates (blue line, above) last year and has been the case in Europe over the past twelve months, in response to rate cuts from the European Central Bank and the Bank of England.

It is potentially noteworthy that a move higher in longer-term rates was not the initial market reaction to Powell’s Jackson Hole speech, as the yield on the 10-year Treasury note actually declined from 4.32% to 4.26% on the day. That said, Chairman Powell also used that speech to caution that "the effects of tariffs on consumer prices are now clearly visible", that the Fed expects those price increases to "accumulate over the coming months" and that “we cannot take the stability of inflation expectations for granted”. 4

President Trump has continually added more and more tariffs, which we believe calls into question the premise that the tariff-related increase in inflation is a transitory phenomenon. Liz Ann Sonders, Chief Investment Strategist at Charles Schwab, agrees, citing the erratic and politically driven nature of tariff implementation in recent years. She notes that “the problem is, there is no ‘one time’ when it comes to tariffs…Their application has been inconsistent—sometimes imposed, sometimes delayed, and often leveraged as a geopolitical or economic tool beyond trade balances or revenue generation. This creates a rolling, ongoing effect.”

She likens it to what she has previously described as a “rolling recession,” where economic weakness does not strike all sectors simultaneously. Instead, pockets of the economy contract at different times, creating a staggered slowdown. That same stop-and-start rhythm, she argues, is now showing up in inflation data. 5

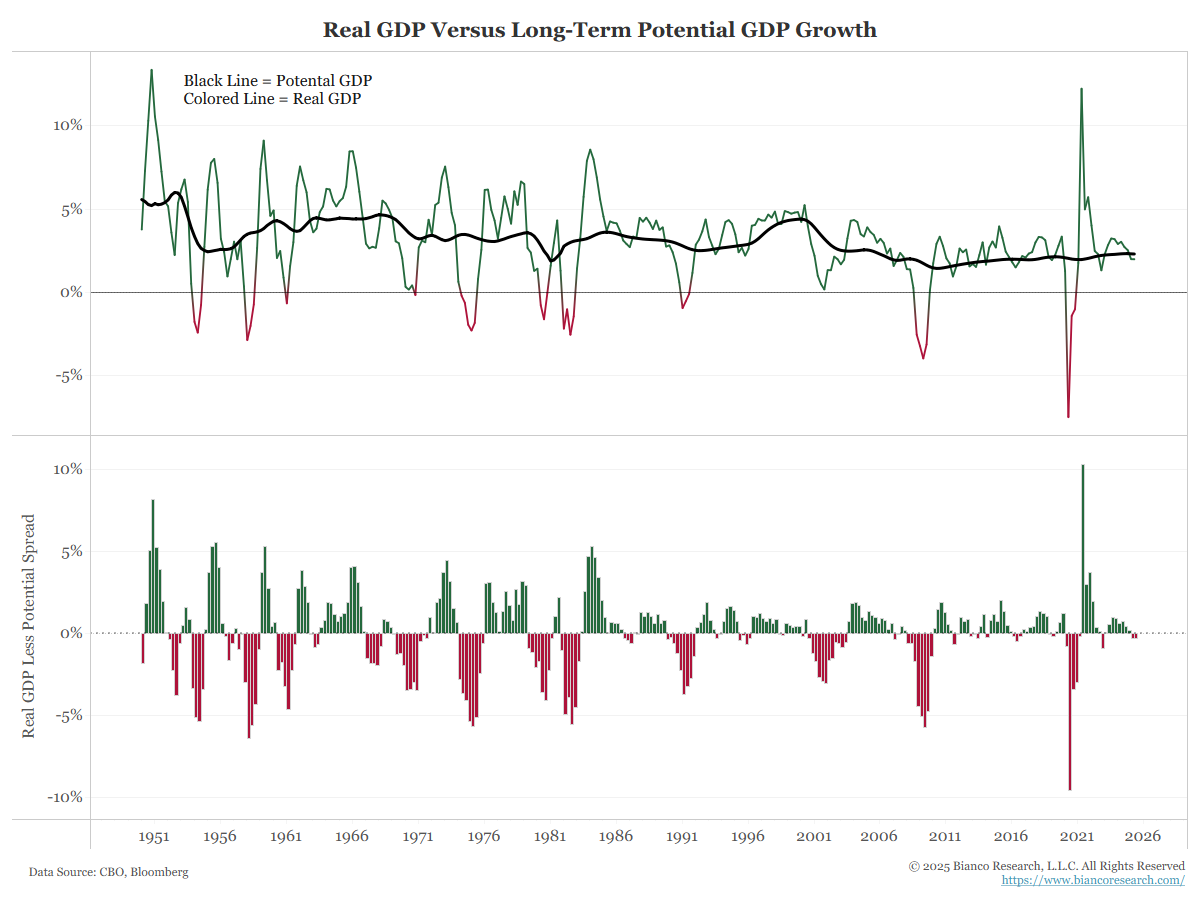

One reason that we are concerned that the Fed is caving to political pressure rather than responding to economic weakness is that the Fed appears ready to lower rates at a time when the economy is already growing close (green/red line on the top half of the above chart) to the level of sustainable, non-inflationary growth (black line on the top half of the above chart).

Moreover, the Atlanta Fed GDP Nowcast, which is the most widely respected of the Fed’s estimates of current growth, is currently projecting a third quarter real growth rate (growth less inflation) of 2.3% 6, which is well above current estimates of sustainable, non-inflationary potential. That does not even take into consideration the trillions of dollars of fiscal stimulus that is being pumped into the economy because of the One Big Beautiful Bill Act. These are among the reasons why we are worrying more about inflation than stagflation.

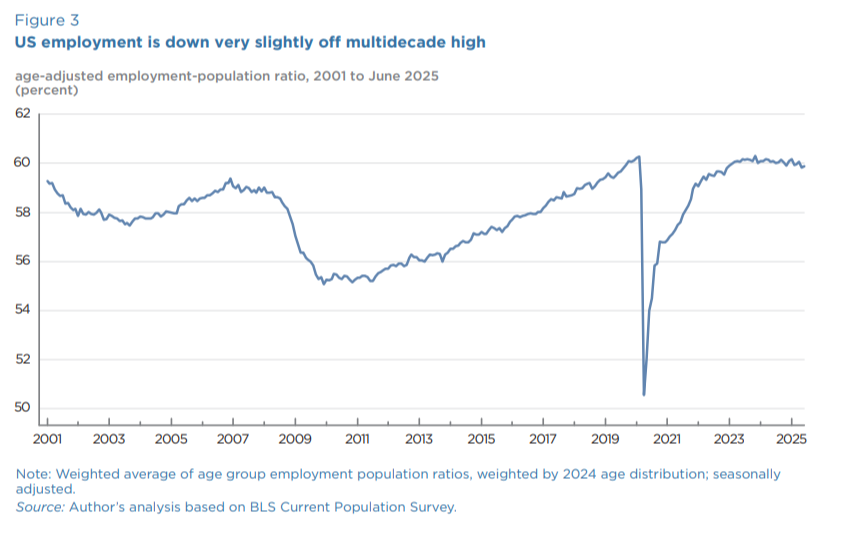

Further, we don’t even think that the labor market is particularly weak, as the unemployment rate is largely unchanged 7, the employment to population ratio is barely below multi-decade highs (below) and the ratio of available jobs to available workers is almost in balance (less than one available worker for every available job). 8

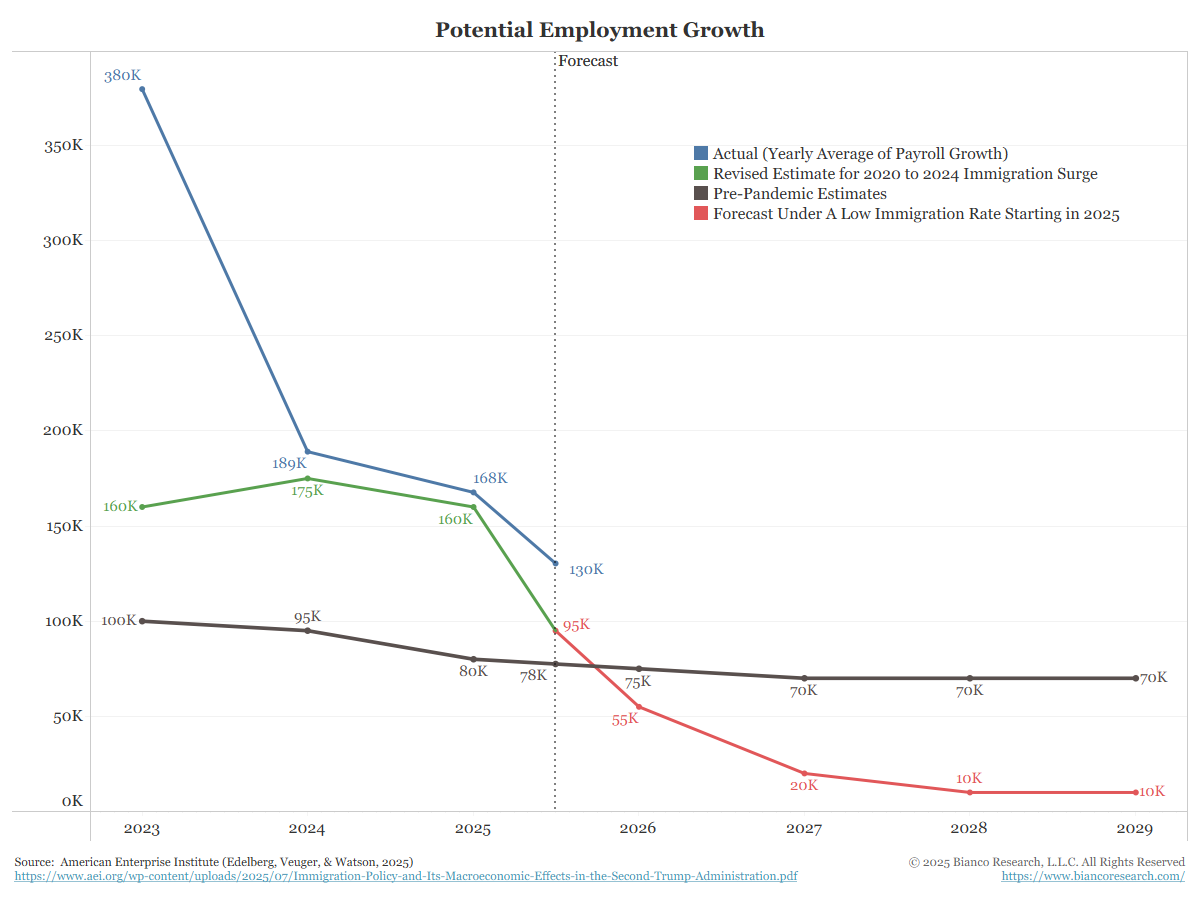

To the contrary, we attribute the poor payroll growth numbers to the dramatic drop in the availability of foreign workers, which limits the economy’s ability to add new jobs (red line below). As Chairman Powell noted at Jackson Hole, “overall, while the labor market appears to be in balance, it is a curious kind of balance that results from a marked slowing in both the supply of and demand for workers”. 9

Chairman Powell’s speech suggests that the Fed is increasingly accepting of the Trump administration’s claim that the tariffs will have an only transitory impact on inflation. That said, we remain mindful that the last time the Fed thought that the inflationary impact of an external shock would be “transitory” was during the supply chain shock of the pandemic, and yet that produced one of the largest surges in inflation in the last fifty years.

While there should be some powerful offsets to higher inflation, including falling shelter costs and artificial intelligence-driven improvements in productivity, we are concerned that a combination of tariffs, a falling dollar, lower interest rates, massive fiscal stimulus, a rapidly shrinking labor force, and an economy that is already running close to non-inflationary capacity seems likely to produce an accelerating and increasingly inflationary economy.

This opinion was reinforced in the just-released minutes from the Federal Reserve’s July 29th-July 30th meeting, where “officials acknowledged worries over higher inflation and weaker employment, but a majority of the 18 policymakers in attendance ‘judged the upside risk to inflation as the greater of these two risks’”. 10

If longer-term interest rates move notably higher in response to the lowering of short-term interest rates, it would likely be a headwind for almost all asset classes (except perhaps the dollar). However, if the move higher in longer-term rates remains within current investor expectations, it should be only a modest negative for debt and fairly benign for the equity markets, particularly in light of the very impressive profit growth currently being enjoyed by most U.S. companies. This outcome seems reasonable, at least until President Trump gets to appoint a new Fed Chairman in May of next year, at which point things could become very unpredictable. Largely due to that uncertainty, we would continue to emphasize shorter maturity and higher-quality debt, with a preference for corporate debt over government debt.

In regard to equities, it would not surprise us if a resumed Fed easing cycle was the catalyst necessary to broaden this current bull market beyond what has largely been large-cap growth stocks and large, money center bank stocks, and into small and mid-cap stocks and the more cyclical and value-oriented parts of the stock market.

While we remain quite bullish for the foreseeable future on most global equity markets, we will close with a point worthy of consideration from State Street head of macro strategy Michael Metcalfe, who noted that “since 1990, world stocks have fallen by an average of 15% at times when U.S. manufacturing activity data showed both a contraction and higher than average prices” 11. While we worry less about economic growth, we think that it will be important to keep an eye on both growth and inflation and believe that the inflation numbers will be a particularly important driver of both monetary policy and portfolio values.

Disclosures

Advisory services offered through Per Stirling Capital Management, LLC. Securities offered through B. B. Graham & Co., Inc., member FINRA/SIPC. Per Stirling Capital Management, LLC, DBA Per Stirling Private Wealth and B. B. Graham & Co., Inc., are separate and otherwise unrelated companies.

This material represents an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor.

Nothing contained herein is to be considered a solicitation, research material, an investment recommendation or advice of any kind. The information contained herein may contain information that is subject to change without notice. Any investments or strategies referenced herein do not take into account the investment objectives, financial situation or particular needs of any specific person. Product suitability must be independently determined for each individual investor.

This document may contain forward-looking statements based on Per Stirling Capital Management, LLC’s (hereafter PSCM) expectations and projections about the methods by which it expects to invest. Those statements are sometimes indicated by words such as “expects,” “believes,” “will” and similar expressions. In addition, any statements that refer to expectations, projections or characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. Such statements are not guarantying future performance and are subject to certain risks, uncertainties and assumptions that are difficult to predict. Therefore, actual returns could differ materially and adversely from those expressed or implied in any forward-looking statements as a result of various factors. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the views of PSCM’s Investment Advisor Representatives.

Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted.

Investing internationally carries additional risks such as differences in financial reporting, currency exchange risk, as well as economic and political risk unique to the specific country. This may result in greater share price volatility. Shares, when sold, may be worth more or less than their original cost.

Definitions

The Standard & Poor's 500 (S&P 500) is a market-capitalization-weighted index of the 500 largest publicly-traded companies in the U.S with each stock's weight in the index proportionate to its market. It is not an exact list of the top 500 U.S. companies by market capitalization because there are other criteria to be included in the index.

Indices are unmanaged and investors cannot invest directly in an index. Unless otherwise noted, performance of indices does not account for any fees, commissions or other expenses that would be incurred. Returns do not include reinvested dividends.

The Consumer Price Index (CPI) is a measure of inflation compiled by the US Bureau of Labor Studies.

Citations

(1) “What US stagflation risks mean for world markets”, Naomi Rovick, Alun John, Posted 8/18/2025 https://www.msn.com/en-us/money/markets/what-us-stagflation-risks-mean-for-world-markets/ar-AA1KIZQw?ocid=hpmsn&pc=AV01&cvid=60ef31ca7

(2) “Ex Fed Pres. Parker Harkers: The data is fuzzy. It is not crystal clear.”, Greg Michalowski, Posted 8/22/2025, https://investinglive.com/centralbank/ex-fed-pres-parker-harkers-the-data-is-fuzzy-it-is-not-crystal-clear-20250822/

(3) “Monetary Policy and the Fed’s Framework Review”, Jerome H. Powell, Posted 8/22/2025, https://www.federalreserve.gov/newsevents/speech/powell20250822a.htm

(4) “Monetary Policy and the Fed’s Framework Review”, Jerome H. Powell, Posted 8/22/2025, https://www.federalreserve.gov/newsevents/speech/powell20250822a.htm

(5) “Unusual Prospect of a Full-Employment Recession Per BlackRock and Charles Schwab”, The Wealth Advisor, Posted 8/13/2025, https://www.thewealthadvisor.com/article/unusual-prospect-full-employment-recession-blackrock-and-charles-schwab?mkt_tok=NjY2LVBIQS05NTgAA

(6) “GDP Now”, Federal Reserve Bank of Atlanta, As of 8/26/2025, https://www.atlantafed.org/cqer/research/gdpnow

(7) “THE EMPLOYMENT SITUATION — JULY 2025”, Bureau of Labor Statistics, Posted 8/1/2025, https://www.bls.gov/news.release/pdf/empsit.pdf

(8) “Graphics for Economic News Releases”, Bureau of Labor Statistics, Posted 7/29/2025, https://www.bls.gov/charts/job-openings-and-labor-turnover/unemp-per-job-opening.htm

(9) “Monetary Policy and the Fed’s Framework Review”, Jerome H. Powell, Posted 8/22/2025, https://www.federalreserve.gov/newsevents/speech/powell20250822a.htm

(10) “Fed Minutes Show Majority of FOMC Saw Inflation as Greater Risk”, Maria Eloisa Capurro, Posted 8/20/2025, https://www.bloomberg.com/news/articles/2025-08-20/fed-minutes-show-majority-of-fomc-saw-inflation-as-greater-risk?sref=YfRIauRL

(11) “What US stagflation risks mean for world markets”, Naomi Rovick, Alun John, Posted 8/18/2025 https://www.msn.com/en-us/money/markets/what-us-stagflation-risks-mean-for-world-markets/ar-AA1KIZQw?ocid=hpmsn&pc=AV01&cvid=60ef31ca7